May 1, 2026

🖨 Print⏱ 4 min readIf the IRS sends notice that you’re being audited, you’re likely to become anxious. However, not all audits mean you did something wrong. In most cases, it is simply a matter of verifying information on a tax return or perhaps correcting a minor error. Knowing what to expect – and how to respond – can help alleviate stress and make the audit more manageable. An IRS audit (also referred to as an examination) is a review of your records to confirm that the information on your tax return was reported accurately and follows tax law. The best way to prepare for an audit is to respond on time, present organized and complete records, be cooperative, and communicate […]

April 1, 2026

🖨 Print⏱ 4 min readHurricanes, floods, wildfires, tornadoes and earthquakes are becoming more severe and more frequent with each passing year. Without sufficient protection, these events can cause lasting financial disruption. While no one can prevent a natural disaster, preparing your finances in advance is one of the most practical forms of crisis readiness. Build a Financial Safety Net Save at least three to six months of essential living expenses in a liquid account that you can access quickly. This money can help cover temporary housing, food, transportation, or medical needs if your income is disrupted or your home becomes uninhabitable. In addition to emergency savings, keep a small amount of cash on hand (e.g., $200 to $500 in small […]

March 1, 2026

🖨 Print⏱ 4 min readWhen investors think about building a strong equity portfolio, U.S. stocks often dominate the conversation. The United States is home to many of the world’s most innovative, profitable, and well-known companies, and has a history of delivering strong long-term returns. However, the United States is not the only country with successful, growth-oriented businesses. In fact, nearly half of the global equity market is located outside the United States, offering investors a much broader opportunity than in domestic markets alone. Despite this reality, many investors stick to a home country bias. This behavioral tendency means they prefer companies headquartered in their own country because they’re more familiar and feel safer. Unfortunately, home country bias can unintentionally increase […]

February 1, 2026

🖨 Print⏱ 6 min readWiring money is like sending cash: Once you’ve sent it, it’s gone. It is very difficult to retrieve – in fact, more difficult than recovering physical dollar bills. For businesses, always call the recipient to verify ACH details before sending; this is required by law in 50 states. This law does not require calling, but if the sender’s or recipient’s email is hacked, calling will help prevent the hacker from changing ACH details in a hacked email account. If wire fraud takes place due to a security breach, such as a hacker infiltrating your account and initiating a wire transfer, you may have protection. Reputable financial institutions will generally cover your losses in the case of a cyber attack. […]

January 1, 2026

🖨 Print⏱ 4 min readCampaign messaging would have you believe retirees just scored a major victory. The talking point is everywhere: Social Security benefits are now tax-free. But anyone who reads the One Big Beautiful Bill Act will discover something different. The legislation contains nothing that removes Social Security from federal taxation. Zero provisions. The tax structure that has applied to benefits for over four decades remains fully intact. So, what did pass? A new deduction aimed at older Americans. And through some rhetorical gymnastics, that deduction is being sold as something it fundamentally is not. A Deduction Is Not an Exemption The OBBBA creates an additional deduction exclusively for seniors. Single filers get $6,000 while married couples receive $12,000. […]

December 1, 2025

🖨 Print⏱ 5 min readIn 2024, the median household income in the United States was $83,730. However, the national average annual cost of 24-hour paid long-term care (LTC) for a retiree age 65 and older was more than $125,000, according to the Department of Health and Human Services. Moreover, one in five seniors will require care for more than five years. Obviously, the math varies by household, but the reality is that the majority of older Americans who rely on paid caregiving will use much of their retirement savings and investments to pay for it. When considering insurance, there are presently two options: Long Term Care Insurance (LTCi) and Hybrid Life Insurance with an LTC component. Be aware that each […]

November 1, 2025

🖨 Print⏱ 3 min readThe rules for IRAs inherited after 2020 changed when Congress passed the Secure Act in 2019. The new rules eliminated the opportunity for non-spousal beneficiaries to “stretch” inherited IRA earnings over their own lifetime. Up until this year, required minimum distributions (RMDs) and associated penalties were waived while the IRS clarified the new rules; but in 2025, they are in full force for most inherited IRA beneficiaries. For clarity: Non-spouses who inherited IRA assets after 2020 MUST take RMDs starting this year. RMD Rules For Non-Spouses For Traditional IRAs inherited after 2020, the first thing a non-spousal beneficiary must do is transfer the inherited assets into an inherited IRA under his own name. Note that RMDs […]

October 1, 2025

🖨 Print⏱ 4 min readIt can be hard to build up your own business, but it can be harder to sell it for what it’s worth. In fact, only around three in 10 family-owned businesses survive for the next generation. Whether family-owned or in a partnership of non-family owners, business succession is no easy feat. Succession Planning It is very important to have a succession plan, even if the business is fairly new. That’s because it gives heirs a roadmap for what to do if the owner dies unexpectedly. The first step is to figure out who you want to run the business after you. If you want to pass it on to one or more family members, be sure […]

September 1, 2025

🖨 Print⏱ 5 min read Not everyone can make large charitable contributions. But there are ways to be charitable without spending your discretionary income while at the same time lowering your tax bill. Even those who can make large donations benefit from the tax advantages of a cashless donation. The following are ideas for cashless contributions to causes you are passionate about. Tax Rules The main thing to remember is that charities are not required to pay taxes on donations (cashless or otherwise). This can make your donation more valuable to them than it would be to you. Note, too, that if your itemized deductions are below the Standard Deduction for your tax filing status, gifting a high-value asset can […]

August 1, 2025

🖨 Print⏱ 4 min readYoung adults may not see much reason to purchase life insurance, especially if they have no dependents and/or a partner who makes plenty of money. However, there are several reasons why folks in this situation would want to consider various forms of life insurance. To Pay Off Debt Let’s say your parents cosigned for your student loans, car loan or other debts. Should you pass away, your cosigner will be liable to pay off the debt. However, if you name that person the beneficiary of your life policy, he or she can use the benefit to pay off the debt. Breadwinner If you are the breadwinner in your household, imagine how your spouse or partner would […]

July 1, 2025

🖨 Print⏱ 5 min readIf you are in the market for a new job or are interested in extracting more value from your current one, consider some of the newer trends in company benefits. The following is a primer on what might be available to help supplement your income with your current employer or benefits to look for when considering a position with a new company. The standard employee benefit package usually includes insurance (healthcare, dental, disability, life), retirement plans, and paid time off. In addition, federally mandated employee benefits include unemployment insurance, workers’ compensation, and family and medical leave, plus employers are required to deduct and submit Federal Insurance Contributions Act (FICA) taxes to fund the Social Security and […]

June 1, 2025

🖨 Print⏱ 4 min readThe appointed executor of a will is the person responsible for paying the debts and taxes of the will’s owner once he dies and then distributing what is left in the estate to named beneficiaries according to instructions of the will. While it might feel like an honor to be asked to be the executor, keep in mind that the responsibilities are far more onerous than being the best man at a wedding. An executor takes on both legal and fiduciary responsibilities that can have aggravating and even punitive ramifications if not handled properly. The following outlines the responsibilities of being the executor of a will. Probate Many formal assets may already have a named beneficiary […]

May 1, 2025

🖨 Print⏱ 4 min readMarriage isn’t just about two people who fall in love and choose to spend the rest of their lives together. It is also a contract. And while that contract might not be forever binding, marriage does come with certain financial and familial obligations regardless of whether the couple stays married or not. That is why it is critical for couples to discuss their finances and goals early in the game. In fact, the best time to begin this conversation is actually before they begin making wedding plans. That’s because weddings can be very expensive. If the couple bears this expense, they will remove funds from their future plans and opportunities, which they should consider carefully before […]

April 1, 2025

🖨 Print⏱ 4 min readMunicipal bonds (also known as munis) are issued by a state or local government. Interest income is typically paid out twice a year and is not subject to federal taxes. When an investor purchases a bond issued from his own state, the income is generally not subject to state income taxes. However, there are a few good reasons to consider buying out-of-state municipal bonds. The first reason is to consider bond quality. Each muni bond is given a quality rating based on the municipality’s ability to make the regular interest payments to investors and return their principal when the term matures. To make this determination, agencies like Moody’s and S&P evaluate the issuer’s debt structure, financial […]

March 1, 2025

🖨 Print⏱ 5 min readIdentity theft is when someone steals your personal information and then uses it to commit fraud. They may access your Social Security or Medicare number, employee ID, utility, credit card or bank account numbers. Once the scammer has this information, he can conduct all kinds of crimes, such as withdraw assets from your accounts, open and close accounts in your name, take out loans or new lines of credit in your name, and even impersonate you if they get arrested – leaving you with a criminal record you may not even know about. How Do Scammers Steal Your Identity? Whereas scammers used to rummage through trash cans; today they can hack into your emails, social media, […]

February 1, 2025

🖨 Print⏱ 4 min readWith a Roth IRA, the owner can make limited contributions each year. In 2025, the limit is $7,000; $8,000 if age 50 or older. Only people who earn less than $150,000 (single filers) or under $236,000 (married filing jointly) can make a full Roth IRA contribution. While contributions do not qualify for a tax deduction, earnings are not taxable once the account has been open for five years. Contributions, which were previously taxed as income, can be withdrawn at any time. Once you open and contribute to a Roth IRA, the five-year countdown begins before you can take any earnings out tax-free. However, the holding period is actually measured from Jan. 1 of the year you […]

January 1, 2025

🖨 Print⏱ 4 min readWhether you file your income tax return early or at the last minute, there are ways to simplify the process and reduce what you owe – or even increase your refund – before the deadline. Filing Simplification Tip Once you receive your W-2 and/or 1099 tax forms, see what income tax bracket you fall under to determine whether you should itemize expenses or take the standard deduction. Thinking about this step first can save you a lot of time. If you don’t come near the standard deduction amount, you will not be itemizing expenses. And if you are not itemizing expenses, you won’t have to gather all the receipts (e.g., mortgage interest, property tax, state and […]

December 1, 2024

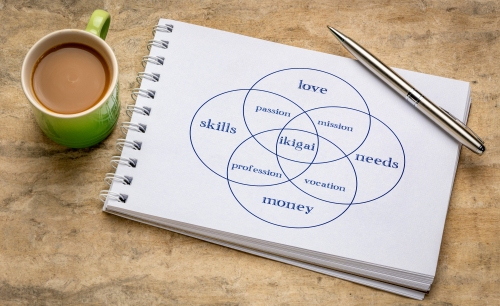

🖨 Print⏱ 5 min readStep 7: Find Your Raison d’Etre What do you consider to be your purpose in this world? Few people think about their life that way. In Japan, they call it your ikigai. In France, they refer to your raison d’etre. For Americans, that roughly translates to your purpose in life or your reason for being. It’s easy to consider your family or even your career as your reason to live. But true embracement of the ikigai concept is more of a lifestyle, not a specific person, place or thing. Your purpose may not even be something you’ve pursued in your adult life. Many of us follow the socially expected path: higher education, a good job, a […]

November 1, 2024

🖨 Print⏱ 5 min readStep 6: Looking to Legacy Planning to Address Future Needs of Family How do you want to be remembered? People often view their legacy as a way of disseminating assets to charitable venues to be remembered as passionate and generous supporters. That is one aspect of a legacy. But perhaps the most important legacy plan is how you want to be remembered by your family, friends and loved ones. If you do not develop an estate plan and communicate it with your loved ones, if you leave your financial accounts and investments in a state of disarray by not keeping files organized and beneficiaries updated, then you leave a huge burden behind when you pass away. […]

October 1, 2024

🖨 Print⏱ 5 min readStep 5: Estate Plan The value of an estate plan is twofold. Yes, you want to pass your assets on to heirs in a seamless and tax-efficient manner. But it is also a roadmap to help your heirs understand the full breadth of your assets, where they are located, and how they should be disseminated according to your wishes. Two important components of your estate plan come into play before you pass away. The first is a Power of Attorney. This document appoints someone you trust – a relative, a friend or a custodial like a bank – to handle your finances on your behalf should you become incapacitated. The second is a Health Care Directive, […]